The Federal Reserve’s Z1 data on American debt (public and private) is out for 2014,

http://www.federalreserve.gov/releases/z1/current/

and I took a look to see how much of our current recovery is just more debt fueled consumption. More selling out our personal and collective futures to maintain our standard of living despite growing inequality, and inadequate savings and investment. More fake prosperity based on paying workers less, yet selling more to them, and importing more than we export, with these imbalances fueling excessive and unearned executive pay.

Everyone knows this has to change sooner or later. The entire house of cards was collapsing in 2008 before the federal government stepped in, at great cost, to keep the game going a while longer. To buy time so Americans, businesses and the financial sector could adjust and the imbalances could be rectified. Has that happened? Is this economic expansion on a firmer foundation than the junk bond bubble, the dot.com bubble, and the housing bubble? Let’s go to the videotape and find out.

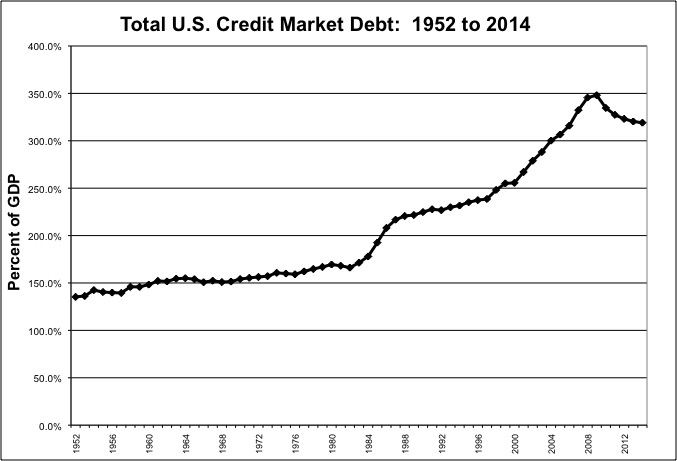

Total U.S. debts (public, private, financial) had been relatively stable during the 1950 to 1980 period, an era when our trade was mostly balanced and the share of national income going to labor was stable as well. Then soaring debts, rising inequality, and a growing external debt as a result of a balance of payments deficit year after year all took place at the same time. Total U.S. debt peaked in 2008. But it has fallen very little since.

So why did the economy get better last year? Financial sector debts – the money financial businesses owe to each other – have been falling as a result of regulations designed to make major banks less prone to crises and in need of bailouts. Although the banks have had some success in Congress reversing those regulations.

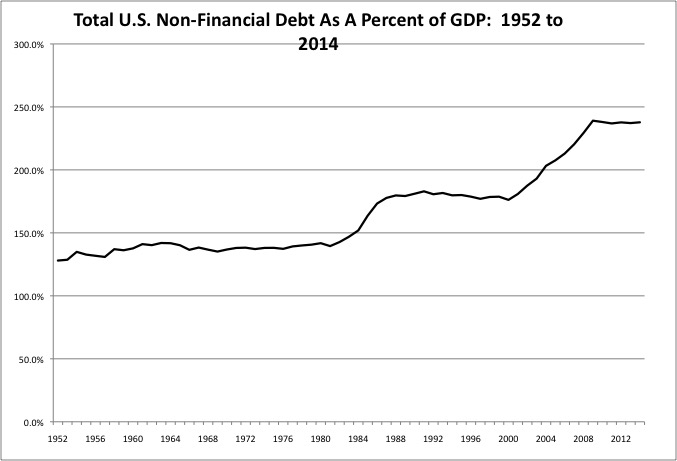

For now financial debts keep falling. Excluding financial sector debts, total U.S. debts actually increased last year, by 0.6% of GDP. It has barely fallen since 2008. To the extent that the U.S. economy survived it was because the debt bubble was kept inflated. To the extent that it got better last year, it is because debts started rising again.

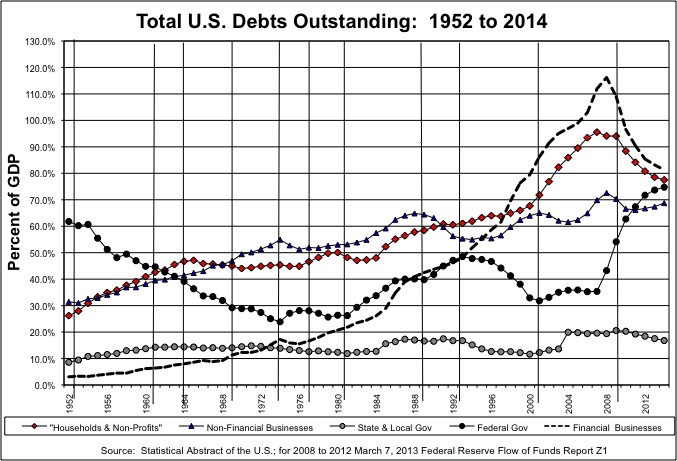

As noted, the federal government stopped the collapse of the debt-fueled economic house of cards by going deep into debt itself. Borrowing hugely for short-term consumption, when individual Americans were too broke to do so individually anymore. Under U.S. bankruptcy law, parents can’t borrow against their children’s future income as individuals. So Generation Greed did so as a group instead. And now, once again, we hear talk of taking federal old age benefits away from younger generations of Americans to pay that debt back. Federal debt increased by 1.0% of GDP in 2014, a slowdown from the rapid debt increase of the prior six years.

State and local government debt has been going down, after it soared from 11.6% of GDP in 2000 to 20.3% of GDP in 2010. That increase in state and local debt, unfortunately, was not to invest in infrastructure – there has been less and less of that – but to balance budgets while putting off painful choices until powerful beneficiaries had been grandfathered in. While on the books debts have started to fall, moreover, the off the books debts of unfunded public employee pension obligations continue to soar, leading to deepening fiscal crises, tax increases and service cuts.

American businesses continue to go deeper and deeper into debt. Not to invest in new productive capacity – why do so when your customers are broke and future sales are doubtful? To buy back stock. This, and zero interest rates, have temporarily inflated stock values, allowing top executives to collect huge bonuses. When stock prices fall back to normal relative to company earnings, all that excess executive pay will once again be shown to have resulted primarily from financial engineering and office politics.

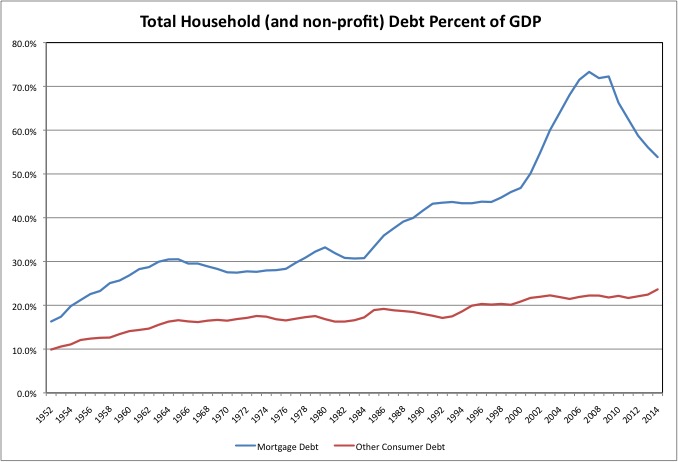

What, however, about American consumers, who dutifully went on spending more than they earned for nearly 30 years, while saving little for retirement? Household and non-profit debt soared to 95.5% of GDP in 2007, but it has since fallen back to 77.5% of GDP. It fell by 1.0% of GDP in 2014, offsetting the increase in the federal debt.

In reality, however, people have not been paying off debts. They have been defaulting on them. Particularly on mortgages, a cost that has been shifted to the federal government. Gradually, over time, banks are pushed to admit their losses and stop carrying unpaid and unpayable mortgages on their books at full value, and that debt is being wiped away in foreclosure. This process knocked mortgage debt down by another 2.2% of GDP in 2014.

Other consumer debts? They are a different story. They increased by 1.2% of GDP last year. There is your economic recovery. Student loans. Auto loans.

Looking at the different parts of the country whose economy I write about, what has been driving economic growth?

First, there is a snapback expansion of the automobile industry and related industries. People basically stopped buying cars during the Great Recession, and the existing cars are wearing out. Trapped in auto-dependent communities, Americans had no choice but to replace those vehicles, particularly with used cars becoming scarce and expensive. But how did they afford it?

http://www.bloomberg.com/news/2015-01-20/honda-warns-against-stupid-auto-loans-driving-u-s-sales-gains.html

A top U.S. executive at Honda Motor Co. (7267) said competitors are doing “stupid things” to boost auto sales, including making seven-year-long car loans that harm buyers.

Automakers are increasingly selling vehicles with 84-month loans that reduce monthly payments while making it tougher to repay faster than cars lose value, John Mendel, Honda’s U.S. sales chief, said in an interview. The Tokyo-based company will avoid longer-term loans even as Nissan Motor Co. (7201) tries to supplant it as the fifth-biggest automaker in the U.S., he said.

“You’re ringing the bell on a new-car sale, but that customer is saddled — they’re stretched so thin,” Mendel said at the North American International Auto Show last week. Extended-term loans are “stupid not just for us, but for the industry.”

The data shows that the auto employment recovery is petering out, along with the ability of people to borrow.

A second growth sector was U.S. oil and gas production, which soared due to advanced “fracking” techniques. But now Saudi Arabia has decided to shut down the U.S. oil industry by slashing prices, making Americans dependent of foreign oil again so prices can be jacked up later. The political response has been deafening silence. No one wants to come out against cheaper gasoline.

http://www.bloomberg.com/news/articles/2014-12-11/fed-bubble-bursts-in-550-billion-of-energy-debt-credit-markets

The danger of stimulus-induced bubbles is starting to play out in the market for energy-company debt.

Since early 2010, energy producers have raised $550 billion of new bonds and loans as the Federal Reserve held borrowing costs near zero, according to Deutsche Bank AG. With oil prices plunging, investors are questioning the ability of some issuers to meet their debt obligations. Research firm CreditSights Inc. predicts the default rate for energy junk bonds will double to eight percent next year.

While the auto snapback is leveling off, the oil and gas boom appears to be heading for a full-blown collapse.

Finally, you have an dot.com/new media/e-commerce boom, including both new firms and existing firms using the new information technology, that has set off extensive job and income growth (and real estate price increases) in major urban centers such as Manhattan/Brooklyn, San Francisco and Boston.

To the extent that new firms, based solely or mostly on the internet, are replacing old ones, as in the media, the newer firms are characterized by lower wages, an absence of non-wage benefits, employees often hired as freelance contract workers, and limited or no profits. And soaring stock prices. But why not invest, when interest rates are close to zero and the dividend yield on the S&P 500 is just 2.0%? What other option is there?

http://finance.yahoo.com/news/mark-cuban-current-tech-bubble-183702507.html

In a recent post on his blog, businessman, investor and Dallas Mavericks owner Mark Cuban compared the current state of the technology market to the dot-com bubble of 2000. According to Cuban, the tech sector is once again in a bubble, but this one is even worse…

While Cuban sees similarities between the current environment and the dot-com bubble, he sees one major difference that makes the modern environment even more dangerous for investors: lack of liquidity. While the dot-com bubble mostly included public companies, the modern tech bubble mostly involves small, private companies.

Some will turn out to be viable long term, just like last time. But a whole lot of money is about to go “poof.” As the “sharks” would say on “Shark Tank,” I’m out.

With young people flowing into selected high education big cities, and blue-collar workers heading for the oil boom states, there is a shortage of housing in many locations despite the remaining surplus of housing elsewhere (from the housing bubble). I was taught, in the mid-1980s, that historically 2 million housing units produced in the U.S. was a big year, 1.5 million was an average year, and 1 million was a deep recession. After a bubble, with one year of 2 million housing units produced after another, and an unprecedented bust, we have now “recovered” to 1 million housing units produced per year. Mostly apartments, and housing in Texas, where an oil bust is now taking shape.

And when average Americans finally got a few extra dollars, they went out to eat at a low cost fast food or fast casual chain restaurant. Or a bespoke place in the cities where the dot.com money is flowing it.

And that, people, is your economic recovery. With two of the three legs on the stool already kicked out.

It wasn’t supposed to be this way. Notes The Economist:

http://www.economist.com/news/leaders/21643188-world-once-again-relying-too-much-american-consumers-power-growth-american-shopper

The American economy is motoring again, to the relief of exporters from Hamburg to Hangzhou…All this is good. But growing dependence on the American economy—and on consumers in particular—has unwelcome echoes…

A decade ago American consumers borrowed heavily and recklessly. They filled their ever-larger houses with goods from China; they fuelled gas-guzzling cars with imported oil. Big exporters recycled their earnings back to America, pushing down interest rates, which in turn helped to feed further borrowing. Europe was not that different. There, frugal Germans financed debt binges around the euro area’s periphery.

After the financial crisis, the hope was of an end to these imbalances. Debt-addicted Americans and Spaniards would chip away at their obligations; thrifty German and Chinese consumers would start to enjoy life for once. At first, this seemed to be happening. America’s trade deficit, which was about 6% of GDP in 2006, had more than halved by 2009.

But now the world is slipping back into some nasty habits. Hair grows faster than the euro zone, and what growth there is depends heavily on exports. The countries of the single currency are running a current-account surplus of about 2.6% of GDP, thanks largely to exports to America. At 7.4% of GDP, Germany’s trade surplus is as large as it has ever been.

China’s growth, meanwhile, is slowing—and once again relying heavily on spending elsewhere. It notched up its own record trade surplus in January. China’s exports have actually begun to drop, but imports are down by more. And over the past year the renminbi, which rose by more than 10% against the dollar in 2010-13, has begun slipping again, to the annoyance of American politicians.

America’s economy is warping as a result. Consumption’s contribution to growth in the fourth quarter of 2014 was the largest since 2006. The trade deficit is widening. Strip out oil, and America’s trade deficit grew to more than 3% of GDP in 2014, and is approaching its pre-recession peak of about 4%.

And when it comes to correcting imbalances, we’re about to strip out oil all right. We’re becoming hooked on cheap imported oil once again.

It may be that all we have achieved by doubling the federal debt as a percent of GDP and keeping interest rates at zero for the better part of a decade is inflating the speculative profits and unearned wealth of those at the top. And allowing some more members of Generation Greed to reach retirement and get “grandfathered” before benefits are slashed for the poorer generations to follow. Postponing, rather than preventing, the reckoning in order to keep the vested interests vested and the paper wealth of the wealthy worth more than the value of paper.

Because the U.S. economy is based, and in fact the world economy is based, on Americans spending more than their employers pay them, until they are broke, foreclosed, and reach old age in poverty with children who are poorer than they had been in their younger days.

I’ll leave you with a link to a discussion I highly recommend. The transcript is also worth reading – the speaker clarified a few thoughts he didn’t put quite the way he wanted in the interview. I don’t recommend reading/listening to many things in full, so if you wonder how I always seem to see what turns out to have been perfectly obvious in retrospect, check this out.

http://moneyweek.com/paul-hodges-interview-the-great-unwinding/

Pingback: The Mets Are New York’s Team, According To State and Local Government Finance Data | Saying the Unsaid in New York()